Price-elasticities — dimensionless parameters that express the extent to which a price increase triggers a usage decrease — are central to policies that aim to reduce a harmful activity by internalizing its damage into its price. The efficacy of carbon fees, congestion tolls, cigarette taxes, and the like turns on the proposition that the toll or tax will dampen consumption by more than a token amount.

If the price-elasticity is close to zero, then the fee devolves to a revenue-raiser that will never fulfill the purpose of reducing the harm. But if there’s at least a modicum of underlying price-responsiveness, then internalizing damage costs via a fee or tax can be a powerful and efficient way of combating pollution, while also raising revenue that can be invested and/or distributed to forestall regressive impacts on lower-income households.

As someone with a long-time orientation toward price incentives and cost internalization, particularly for major sources of environmental damage such as energy use and driving, I’ve made it my business to keep on top of the literature on price-elasticity. Several years ago, in the course of assembling a monster spreadsheet for modeling congestion pricing in New York City, I spent months combing empirical studies of driver responsiveness to changes in tolls, gas prices, and parking charges. Ditto to develop the Carbon Tax Center’s carbon-tax impact model, which subdivides energy use into four sectors — electricity, gasoline, aviation, and “other” — with different estimates of price-elasticity for each.

With this backdrop, consider the strange post this week by The Atlantic business and economics editor Megan McArdle.

McArdle’s piece, “Should We Re-Evaluate Carbon Taxes?,” began well enough:

I’ve long been an advocate of some form of carbon taxation — gas tax, source fuels tax, even cap-and-trade if nothing else is available. The tax seems like a three-fer: raise revenue, discourage use, and encourage innovation.

McArdle has indeed been a staunch carbon tax advocate. Back in 2007, in “The perils of buy local,” she noted the absurdity of making individuals track the carbon footprints of local vs. global food, and concluded:

[I]f we’re serious about cutting carbon dioxide emissions, we need a carbon tax, and not CAFE, or other sorts of piecemeal regulatory solutions.

While I wouldn’t have cast it as either/or, McArdle’s emphasis on a carbon tax is exactly right.

But McArdle’s new piece quickly leaves the rails:

Jim Manzi has been making a pretty compelling argument that [a carbon] tax will do much less than people like me have been anticipating. Even the long-term response to price increases is simply too low.

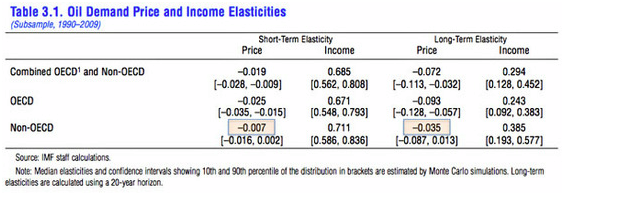

This is weird. For Manzi’s “compelling argument” turns out to be nothing of the sort. Rather than a considered examination of the vast body of studies of energy elasticities, Manzi’s “argument” is a lone table cherry-picked from the International Monetary Fund’s (IMF) new (April 2011) 242-page World Economic Outlook [PDF]. And lifted from the IMF not by Manzi himself but by Mother Jones political blogger Kevin Drum, in a post last Friday, “Everyone Loves Oil,” which in turn was built around a post the same day by peak-oil blogger Stuart Staniford.

OK, no crime in linking to someone else who linked to someone else who linked to someone else. For the goods, let’s go to the IMF table posted by Staniford, Drum, Manzi, and McArdle:

Hmm, looks like an elasticity-killer — on a quick glance. Over the period 1990-2009, the long-term price elasticity of oil demand shown for OECD countries — developed nations like the U.S., Western Europe, and Japan — is a meager 0.093. At that rate, a 40 percent rise in the price of oil would drop consumption by only 3 percent — a paltry impact, and far too small to justify putting a carbon tax at the center of climate policy.

But wait. The actual change in U.S. gasoline consumption over the past two decades tells quite a different story:

- From 1990 to 2010, the real pump price rose 40 percent (I’ve removed general inflation of 67 percent from the 133 percent nominal price rise from $1.22 to $2.84 per gallon; elasticities are calculated on real, not nominal, price changes).

- U.S. gasoline consumption grew by 25 percent over this period, from 7,235,000 to 9,034,000 million barrels a day.

- Real GDP grew by 65 percent.

- Let’s assume that, all things equal, each percent increase in economic activity is accompanied by a half-percent increase in gasoline use (i.e., an income-elasticity of 0.5). This mid-range assumption is more conservative than the 0.67 income-elasticity I’ve assumed for years.

With these inputs, the observed price-elasticity of U.S. gasoline demand over the past 20 years is around 0.20. The simplest way to see this is to observe that, absent price effects, the increase in gasoline usage would have been half of the GDP rise of 65 percent, or 32.5 percent. The actual increase, however, was 25 percent. Dividing the demand “shortfall” of 7.5 percent by the 40 percent real price increase yields an elasticity of around 0.20. (The true elasticity derived from these numbers is (negative) 0.23, since that’s the exponent to which 1.4, the price multiple, must be raised to yield 0.925, the quantity multiple (1 minus 7.5 percent).) That’s twice the long-term elasticity for OECD countries in the IMF table that McArdle et al. relied on.

But this correction to a 0.20 gasoline price-elasticity estimate is just for starters. As everyone knows, the long-term rise in gasoline prices has been more fluctuating than monotonic. Over the past eight years, the month-to-month price has fallen 43 percent of the time [see the “Volatility Graph” tab in this spreadsheet], obscuring the overall upward trend and giving drivers, car-makers and regulators alike a recurring “out” from the task of adapting to higher prices. Thus, the rough gasoline price-elasticity figure of 0.20 almost certainly understates the reductions in gasoline demand that a ramped-up, phased-in carbon tax, with its unambiguous price signal, could deliver.

To its credit, the IMF acknowledges this, in its Technical Appendix that McArdle et al. evidently overlooked:

To examine whether high oil prices are more conducive to substitution away from oil than low oil prices, we split the sample into periods of high and low oil prices … The results (Table 3.4) suggest that during periods of low oil prices, price elasticity is not statistically different from zero … In contrast, during periods of high oil prices, price elasticity is much higher, at 0.38. [p. 132/242. Note also that the figure of (negative) 0.038 in Table 3.4 is a typo; according to an IMF staffer I contacted, the intended figure, matching the text, is 0.38.]

As it happens, 0.38 roughly matches the 0.40 price-elasticity figure I inputted into my carbon-tax impact model. It’s also essentially the estimate of the long-run U.S. gasoline price-elasticity that the Congressional Budget Office proffered in its 2008 report, “Effects of Gasoline Prices on Driving Behavior and Vehicle Markets” [PDF]:

Estimates of the long-run elasticity of demand for gasoline indicate that a sustained increase of 10 percent in price eventually would reduce gasoline consumption by about 4 percent. That effect is as much as seven times larger than the estimated short-run response, but it would not be fully realized unless prices remained high long enough for the entire stock of passenger vehicles to be replaced by new vehicles purchased under the effect of higher gasoline prices-or about 15 years. Over that time, consumers also might adjust to higher gasoline prices by moving or by changing jobs to reduce their commutes-actions they might take if the savings in transportation costs were sufficiently compelling. Those long-term effects would be in addition to consumption savings from short-run behavioral adjustments attributable to higher fuel prices. (p. XI)

It’s also helpful to keep in mind that gasoline is both a minority factor in CO2 emissions (21-22 percent of the U.S. total) and the least-elastic large consuming sector. Gasoline demand is considered less price-sensitive than aviation, for which fuel accounts for a larger fraction of the overall cost than it does for driving; less price-sensitive than electricity, for which efficiency upgrades and behavioral changes provide rich opportunities for conservation; and probably less price-sensitive than home heating, manufacturing, trucking, etc., which my model subsumes under the rubric of “other.” The model assumes price-elasticities of (negative) 0.70 for electricity, 0.60 for aviation, and 0.50 for other, along with 0.40 for gasoline.

To see what these numbers mean, let’s select the (negative) 0.50 elasticity for “other”: A carbon tax that raised the price of heating oil, manufacturing fuels, etc. by 50 percent would be expected to reduce usage by 18-19 percent, since the assumed price multiple of 1.5 (that’s 1 + 50 percent) raised to the negative 0.50 power (that’s the elasticity) is 0.816, which is one minus 18.4 percent. As the carbon tax kept kicking in, a doubled price would reduce usage by nearly 30 percent, since 2 (reflecting the doubled price) to the negative 0.50 power is 0.707. Now we’re getting somewhere.

So McArdle, take heart. And Manzi, Drum, and Staniford, take note: There’s nothing wrong with price-elasticities, and little that a robust carbon tax couldn’t do, in conjunction with smart policies to remove institutional barriers to efficiency and renewable. Stop kvetching, and get on board.

Postscript: As I was posting this piece, a colleague directed me to an April 27 post by Adam Ozimek, “Of carbon taxes and price elasticities“, that makes many of the points offered here … and more elegantly.