The smart energy analysts over at Pike Research — which puts out weekly reports I’d love to see but can never afford — recently published an interesting brief, and for once it’s free! It’s a high-level overview of “Five Metatrends to Watch in 2013 and Beyond” in the energy sector. Metatrends! (I really wanted to call this post “Metatrends Vs. Crocosaurus.” Here they are:

- Energy is becoming increasingly democratized.

- The role of government innovation funds is changing.

- Technologies are converging.

- The Southern African Power Pool is becoming the new BRIC.

- The role of utilities is changing.

Let’s put aside Nos. 2 and 4, fascinating as they are.

Faithful readers know that I’m obsessed with No. 1, the democratization of energy, which refers to more and more consumers also being producers, more and more municipalities taking charge of their own energy, and thus power over power (as it were) devolving into local hands.

But what strikes me is that 1, 3, and 5 are all aspects of the same trend — a METAmetatrend. (Take that, Pike!)

The metametatrend in energy is, for lack of a better term, decentralization. Systems that were once composed of a few big technologies and a few big companies — along with thousands or millions of passive consumers — are beginning to be replaced by recombinant swarms of small producers and consumers engaging in millions of peer-to-peer transactions with a wild and woolly mix of small-scale technologies.

It’s going to be awesome! We have lived through a revolution like this before: the information revolution. I’m old enough to remember a time when it was vastly easier to consume information than to produce and distribute it. Even the internet started as what amounted to a large library, from which individuals downloaded info. But the spread of cheap processing power and bandwidth now means that anyone can produce information — a song, a video, an app, a funny cat picture — and get it in front of millions of people, instantly and virtually effortlessly, for dirt cheap.

The same kind of thing is just beginning to happen in energy. Pike is wise on this:

As [the decentralization of the internet] took over a decade and is ongoing, the process of energy democratization will also take a long time. We will not start to see large impacts on the energy market for some time yet. At present, the democratization of energy is in a phase that is the equivalent of [the internet in] 1996 … Yet, we are cognizant of the potential of this trend in a way that users and developers of the Internet in 2006 were simply not.

This is key: We are very, very early in the process. We’ve only seen hints of what’s to come. It is far too early to know how far it might go or what changes it might bring.

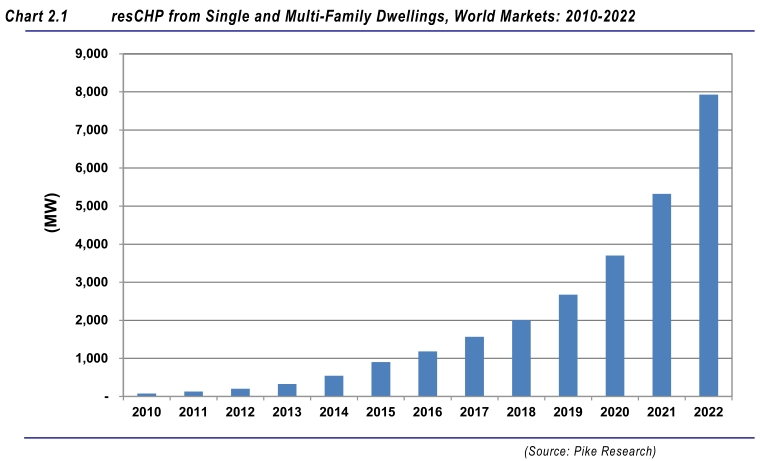

“Small is beautiful” types are somewhat out of fashion these days, as it remains unclear how today’s small-scale distributed technologies could fully cover the energy needs of millions of new developing-world consumers. I’m sure in the early days of cell phones and the internet it wasn’t clear how (or whether) they’d take over the world either. But we’re starting to see adoption curves trending steeply upward, and not just for intermittent sources like solar either. Take residential combined heat and power (resCHP), whereby homeowners or businesses harness the waste heat from their furnaces to generate small amounts of electricity.

Here’s what Pike projects based on current market conditions:

Imagine if the curve bends upward at the same rate for 10 years after that, and 10 years after that. Serious stuff. In a crucial caveat, however, Pike notes that if certain policies and complementary technologies are put in place, “this could be seen as a very pessimistic forecast.”

In other words, this piece of the new energy puzzle will develop faster than projected if other pieces develop along with it. That’s what makes this stuff so hard to predict: There are lots of small pieces, interacting in complicated and sometimes nonlinear ways.

Which brings us to metatrend No. 2, technologies converging. What Pike means by this is that energy technologies (and sources) have traditionally developed independently of each other, but they are starting to combine into “integrated solutions,” pulled along by market demand.

So, for instance, where once a building owner might have bought a furnace from one company, building upgrades from another, and a backup diesel generator from another, she might now be searching instead for a provider of power services. A service provider is not selling particular technologies, it is selling heating, cooling, and/or emergency backup, which it might provide through any of a number of combinations of renewable energy, energy storage, and efficiency upgrades. Service providers compete to provide the best energy services, not the best tech or the cheapest per-kWh energy.

This has always been the promise of small, modular energy technologies, that they would enable robust markets for energy services. It’s a welcome trend because it democratizes energy markets, weakening monopolies and opening up opportunities for clever entrepreneurs who can combine existing technologies and services in new ways. (It helps if policymakers do their part as well.) Whereas one kWh is as good as any other kWh, energy services can be specialized and custom-crafted for niche markets. Service providers have an increasingly diverse array of renewable energy generators, fuel cells, energy storage, and intelligent automization solutions to choose from. The toolbox is getting bigger.

The effects of this market convergence will also be difficult to forecast, for the same reason: It involves dozens of technology, regulatory, and business practices evolving in concert, with unpredictable, emergent network and system effects.

And so we come to metatrend No. 5, the changing role of power utilities:

Electric utilities tend to create natural monopolies because of economies of scale.

However, these monopolies are eroding, and new technologies and business models are poised to take advantage. When the emergence of independent power producers (IPPs), energy service companies (ESCOs), and cooperative energy companies is combined with the growth in feed-in-tariffs for individuals, utilities are (in some cases) transformed from being the central producer, distributor, and controller to being the purchaser and aggregator of power.

That got a little jargony, but the point is, utilities used to be in the business of generating power at big power plants and then sending it to consumers over one-way lines for a set price. That basic “hub and spoke” model is rapidly becoming obsolete. There are more and more small-scale power generators and power storage nodes on the network, sending power back and forth in massively parallel fashion. Utilities cannot hope to centrally manage all those transactions. They will be forced, whether they like it or not, to move to what’s known among nerds as a more “transactive” model, in which their main job is to manage power markets, to dynamically price (value) power so that the market can react accordingly. Smart-grid analyst Jesse Berst explains:

Transactive energy distributes decision-making throughout the system. Devices can be programmed with the “price” they will respond to at different times and conditions. Then they can respond on their own when they see a value signal that matches. When done properly, distributed values incorporate prices and constraints across the system to achieve reliable results. No need for centralized intervention.

Another way of looking at this is, utilities are going to have to get used to power markets behaving more like actual markets. Conservatives ought to love it.

One fascinating aspect of the utility picture is that experimentation and evolution are happening fastest in the developing world, where electric systems are often being built from the ground up.

It is likely that electric utilities in North America and Europe will have much to learn from the utilities that mature in the developing world. In regions currently lacking a central grid, utilities will come to represent flexible and robust machines, instead of the slow-moving giants of the developed world. Ultimately, the system that grants individuals and companies the most stable and least expensive source of electricity will lead the market. This model will likely come from a fresh perspective on how to generate and distribute the electricity that is currently evolving in the developing world.

This is kind of a fancy way of saying that behemoth utilities in the U.S. and Europe are likely to be impediments to change for the foreseeable future.

Anyway, add these three metatrends together — energy being democratized, small-scale technologies converging into new solutions, and utilities being dragged into the 21st century — and you get the metametatrend of decentralization. Energy, power, and control are leaking out of their centralized repositories and spreading out into more hands.

I expect this to have salutary effects on both the pace of innovation and the strength of democracy. It’s a real ray of hope in an energy world that can sometimes seem hidebound and dismal.