(Grist illo; Carlossg/Flickr)

(Grist illo; Carlossg/Flickr)

A typical supermarket’s meat counter displays a landscape of easy bounty: shrink-wrapped chops, cutlets, steaks, roasts, loins, burger meat, and more, almost all of it priced to move.

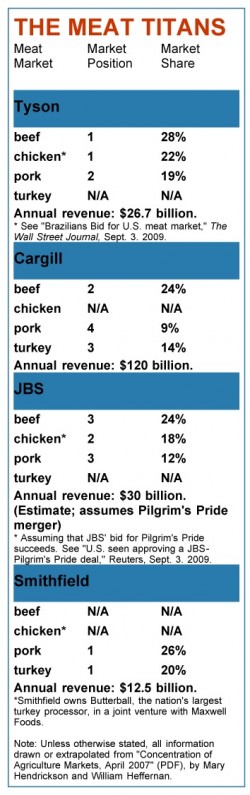

But the dizzying variety cloaks a disturbing uniformity. As the chart below shows, the great bulk of the meat consumed in the United States comes from just four large, powerful companies. These companies wield tremendous power to dictate not just what meat is available, but how that meat is raised.

For these “meat titans,” turning a profit selling cheap meat means slashing the cost of doing business. And that in turn means paying their farmer-suppliers as little as possible for live animals, and paying workers as little as possible to slaughter and process them.

Since the meat market began its dramatic arc of consolidation three decades ago, farmers have had to choose between scaling up, to make up on volume what they were losing on price, or exit the business altogether. As a result, millions of small, diversified farms have closed down their animal-raising operations over the past 30 years, and surviving farms have mostly scaled up, specialized in one species, and placed that species by the thousands in vast confinements known as concentrated animal feedlot operations, or CAFOs. These fragrant, teeming spaces are notorious sources of pollution and social decay in rural areas.

Three of the companies that now dominate the U.S. meat market — Tyson, Smithfield, and Cargill — will be familiar to most readers; the fourth isn’t exactly a household name. Over the last two years, a Brazilian beef-packing conglomerate called JBS has come barreling into the U.S. meat market, taking advantage of a weak dollar and economic troubles among top domestic players.

First, it bought up two prominent beef players, grabbing a nearly quarter of the U.S. beef market. Only Tyson, with 28 percent, has a larger share; the agribusiness giant Cargill is tied with JBS for second place, with 24 percent of the market. Then JBS swooped in and bought two-thirds of chicken giant Pilgrim’s Pilgrim’s pride, giving it 18 percent of the U.S. poultry market, second only to Tyson’s 22 percent. In the course of its dealmaking, JBS also acquired some pork interests, taking 12 percent of that market — putting it in third place behind Tyson (19 percent) and hog king Smithfield (26 percent).

After all of those U.S. deals — and its recent takeover of its former Brazilian beef rival, Bertin — JBS is now the largest industrial-meat purveyor on the planet, bigger in terms of global meat sales than even Tyson and Cargill.

After all of those U.S. deals — and its recent takeover of its former Brazilian beef rival, Bertin — JBS is now the largest industrial-meat purveyor on the planet, bigger in terms of global meat sales than even Tyson and Cargill.

But it might not be quite done getting bigger. According to a rumor published in a Brazilian paper, JBS is hotly pursuing a deal to take over hog giant Smithfield, which has struggled in recent years with volatile feed costs and the bad economy, AP reports.

On Wall Street, Smithfield shares jumped more than 8 percent Tuesday morning on excitement over the news, before settling in with a 1.7 percent gain for the day. That performance, on a dismal day overall for the stock market, shows investors are giving credence to the rumor.

Why would Smithfield submit to being swallowed up by JBS? Well, for its shareholders, the deal makes sense. The company is almost completely dependent on the pork market, which has been hit hard by volatile feed costs and the bad economy for two years now. Being folded into JBS, with its massive poultry and beef positions, would provide a buffer.

For JBS, the deal is a little harder to explain. The U.S. meat market isn’t growing particularly briskly, and profits have been low or nonexistent for two years. I think my analysis of JBS’s Pilgrim’s Pride deal last year applies here as well:

Really, this deal seems to be about exports — a play on rising global demand for cheap meat. Even in the best of times, overall demand for meat in the U.S. is stagnant, rising only at the sluggish rate of population growth. U.S. meat companies boost profits in two ways: 1) by squeezing their suppliers (farmers) on price and slaughterhouse workers on wages; and 2) expanding into foreign markets where growth in meat consumption remains brisk. At this point, the real cash is to be made through access to places like Asia and Eastern Europe, where demand is rising rapidly. And U.S. companies have been masterful at gaining access to those markets — which is probably why JBS is so interested in alighting here.

Even if JBS and Smithfield make a deal, there’s no guarantee the Justice Department will allow it to go through. True, the DOJ approved JBS’ move on Pilgrim’s Pride last year, but the Brazilian behemoth had no U.S. chicken interests at the time. In the current case, JBS does own 10 percent of the pork market; adding Smithfield’s 26 percent would give it a pretty dominant position in pork. The DOJ, already looking askance at the meat industry’s market power over its farmer-suppliers, might just blanch.

As well it should. A JBS/Smithfield tie-up would leave three companies in near-complete control of the U.S. meat market, ramping up pressure on farmer/suppliers to scale up the size of their already-factory-scale animal farms — and reduce their already-lax environmental controls.