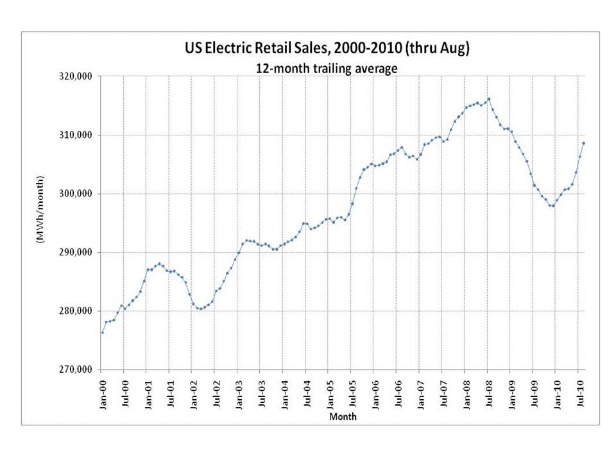

Last July, I wrote about trends in U.S. retail electric sales as an indicator of economic activity, and how this recession compares to prior on that metric. We’ve kept tracking that data, and it gets more interesting with each passing month. Here then, a quick update.

First off, a lament. I wish EIA would update their electric sales more frequently. As of December, their databases are current through August. So whatever happened during the fall remains unknowable, at least for now.

Good news first. The economy continues its recovery, and the rate of that recovery appears to be accelerating.

Retail electric sales aren’t yet back to the trend growth they were on in 2007, but have made up all the ground lost in 2009, recovering faster than they collapsed.

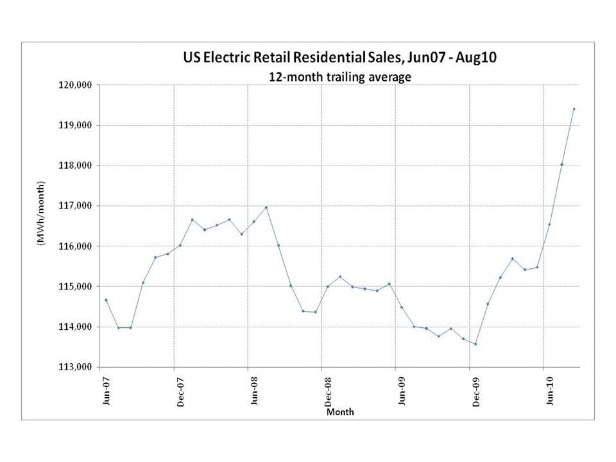

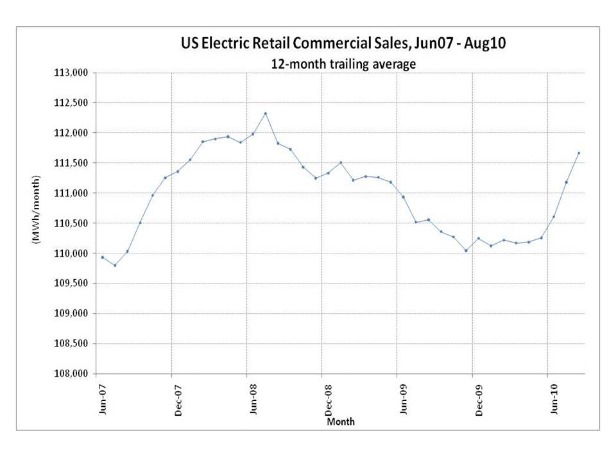

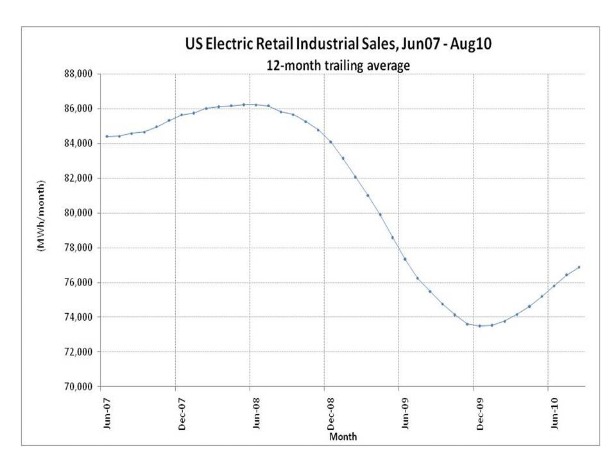

In my prior post, I noted how the recessions have always ended with such recoveries, but the mix of sales has been subtly shifted each time, essentially accelerating the long-term deindustrialization trend of the U.S. economy. All sectors enter U.S. downturns together, but the industrial sector has been less likely to emerge. So far, this recession is continuing that pattern:

The scales are slightly different on these plots to make it easy to read, and on an absolute basis, much of the growth has come from the industrial sector. But on an absolute basis, most of the load destruction happened in the industrial sector — so what’s more interesting to me is the relative gains. In that case, it’s all about residential, and to a lesser degree commercial. The industrial sector is not only still well below their pre-recession purchases, but — unlike the other two sectors — appears to be slowing down. To my eye, that looks like another bout of permanent de-industrialization, which can’t be good news for employment figures.

I’m at a loss to explain the residential data. Pre-recession, we had too many homes, easy credit, rapid construction, booming demand for plasma TVs and other consumer electronics … I get why all that leads to rising residential electric sales. But the data is showing that as of this summer, we were at all time highs for residential electric sales. Maybe there’s a seasonal impact, but all these data-points are on a trailing-12-month basis, so that can’t be a huge effect. I’m at a loss to square that with housing vacancy rates, unemployment and slower consumption. Any ideas?

What remains clear is that while the economy is rebounding, it is simultaneously restructuring, becoming ever-less dependent on industrial activity. That troubles me, for what it says about the long-term prospects of the U.S. economy.